- Published on

The Curious Case of Gold - Part 1: The Rise

- Authors

Something strange happened in 2025. Gold - the metal that does nothing, earns nothing, and just sits there glinting - outperformed the S&P 500, Bitcoin, and almost every other asset class on the planet. It set 53 all-time price records in a single year. It crossed $4,000, then $5,000, and briefly touched $5,600 an ounce before one of the most spectacular single-day crashes in commodity market history.

This is Part 1 of a three-part series. Here, we focus on the rise: what happened, why it happened, and what the extraordinary run-up reveals about the world we're living in. Part 2 will dig into the crash. Part 3 will ask the uncomfortable question: what comes next?

Table of contents

- A metal that does nothing

- The numbers, in context

- The confluence of forces

- Central banks: the quiet buyers

- The geopolitical engine

- Silver's wilder ride

- Where we stood going into 2026

A metal that does nothing

Warren Buffett famously hated gold. His argument was simple: it just sits there. You dig it out of the ground, melt it into bars, and then bury it in vaults again. It produces no earnings, pays no dividends, and generates no cash flow. In a world where capital compounds, gold just... gleams.

He wasn't wrong. Over long stretches of history, stocks comfortably beat gold. The S&P 500's average annual return since 1971 is around 10.7%. Gold's is 7.9%. On that basis, gold looks like the underperformer it is supposed to be.

But here's the thing: gold is not competing with stocks. It is competing with distrust. It goes up when people stop believing in governments, currencies, and institutions. And by that measure, 2025 was gold's year in a way that had not been seen in nearly half a century.

The numbers, in context

To understand how extraordinary the 2025 rally was, you need to zoom out.

Gold Price: Year-End USD per Troy Ounce (2000–2025)

In the year 2000, an ounce of gold cost $273. By the end of 2025, it cost $4,310 - with an intraday peak of $5,600 in late January 2026. That is a 1,479% increase over 25 years. Put another way: if you had bought £10,000 worth of gold at the turn of the millennium and done absolutely nothing, you would have over £150,000 today.

But the pace in 2025 was something else entirely. Gold rose from roughly $2,600 at the start of the year to over $4,300 by year-end - a 65% gain in twelve months. The World Gold Council recorded 53 new all-time highs over the course of the year. The last time gold posted annual gains of this magnitude was 1979, the year before its all-time inflation-adjusted peak.

The move from $3,500 to $4,000 took just 36 days. The move from $4,000 to $5,000 took a little longer, but the direction was relentless. In January 2026, as the market entered a state of near-euphoria, gold briefly crossed $5,600 - before everything fell apart. But that is Part 2's story.

The confluence of forces

No single event explains gold's rise. What made 2025 different was the convergence of multiple, mutually reinforcing forces - some familiar, some genuinely new.

The dollar problem

Gold and the US dollar share an inverse relationship that is as old as modern financial markets. When the dollar weakens, gold rises. When real interest rates fall - meaning the interest you earn after accounting for inflation - gold becomes comparatively more attractive, because the "cost" of holding something that earns nothing shrinks.

In 2024 and 2025, the Federal Reserve began cutting rates in earnest. The first cut came in September 2024, a 50-basis-point move that surprised markets with its aggression. By the end of 2025, the Fed had cut three times, the dollar had weakened significantly from its 2022 peaks, and real yields had been pushed lower. Each of those conditions was independently bullish for gold. Together, they were rocket fuel.

Trump's tariffs and the uncertainty premium

In early 2025, the Trump administration began implementing a sweeping programme of tariffs - on European allies, on Chinese goods, and on a range of imports that sent tremors through global trade relationships. Markets hate uncertainty more than they hate bad news, and the tariff agenda delivered uncertainty in industrial quantities.

When global trade relationships fracture, investors look for somewhere to park capital that is not tied to any one country's policy. Gold, which sits outside the financial system, carries no counterparty risk, and cannot be sanctioned or devalued, becomes that place. There was a telling detail in Q1 2025: the Bank of England reported a significant spike in physical gold being moved from London vaults to US depositories, as traders rushed to hold bullion in America ahead of potential tariffs on precious metals imports. The volumes were large enough to cause actual disruption in gold lending markets.

The debt spiral backdrop

There is a slower, deeper force at work beneath all of this. The United States national debt is approaching $36 trillion. Annual interest payments on that debt now exceed $1 trillion - more than the entire defence budget. Budget watchdogs have warned of a "debt spiral" in which borrowing costs begin to exceed economic growth, making the debt self-compounding.

Gold is, in part, a bet on this scenario. When bond markets worry that a government's debt is genuinely unsustainable, the traditional safe-haven - US Treasury bonds - becomes part of the problem rather than the solution. One strategist put it plainly during 2025: "The bond market understands that Washington is so broken and the debt situation is so bad that gold is the safe haven now, even more than Treasuries. I don't think a lot of people ever thought they'd see that again."

The ETF effect

One structural change that has permanently altered gold's market dynamics is the exchange-traded fund. Before the first gold ETF launched in 2004, buying gold meant physically acquiring it - bars, coins, storage, insurance. The ETF removed all of that friction. Now anyone with a brokerage account can buy and sell gold exposure in seconds.

The result is that gold ETFs have created an entirely new class of buyer: large institutional funds that track gold as part of a portfolio allocation rather than a conviction trade. In 2025, ETF inflows were the highest since the first half of 2020, during the Covid panic. North American gold ETFs alone held almost $200 billion by October. When that much institutional money moves into a single commodity, price effects are significant.

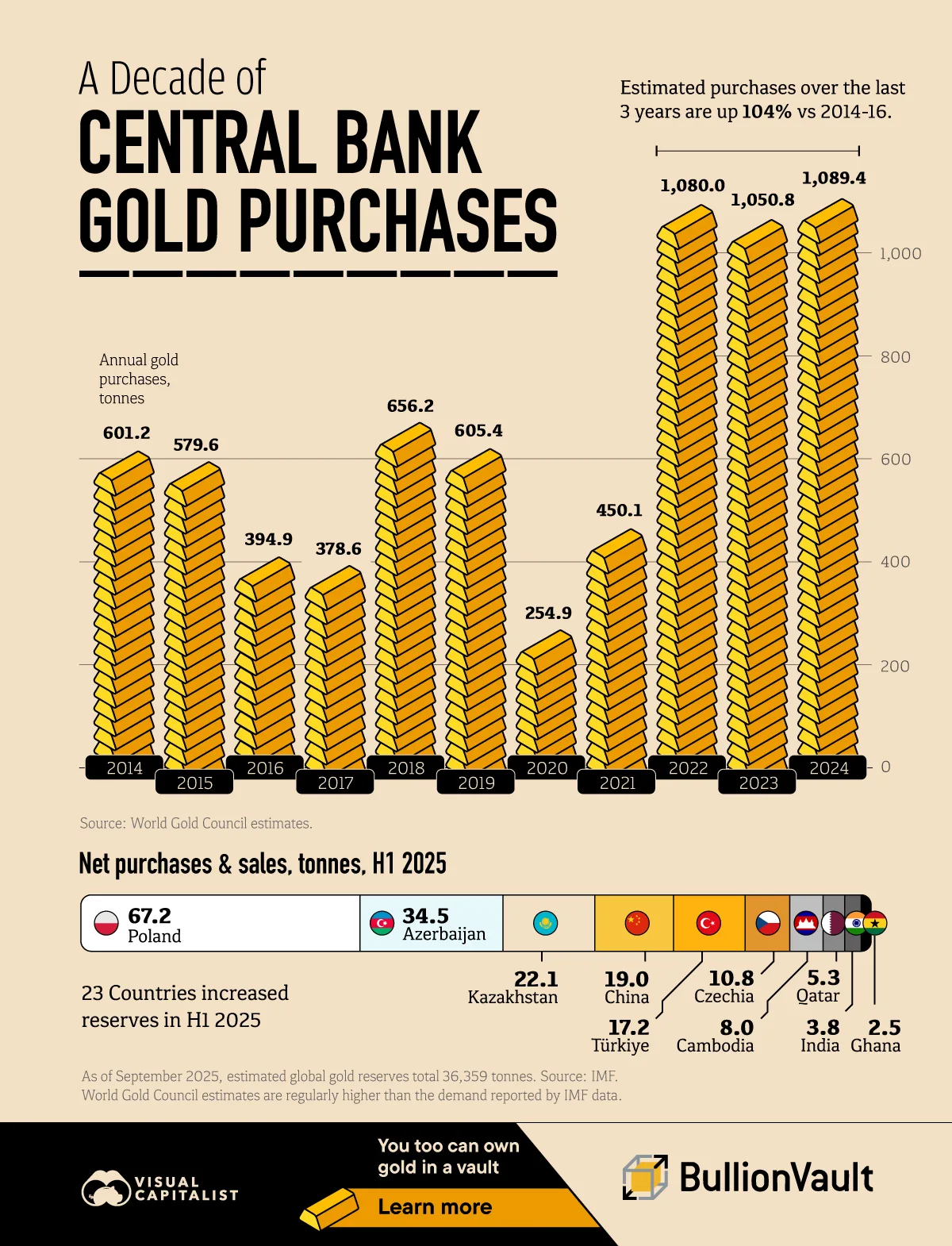

Central banks: the quiet buyers

If the ETF demand was visible and loud, what was happening in central bank vaults was quieter - and arguably more consequential.

Central Bank Gold Purchases: Annual Net Buying (Tonnes)

For fifteen consecutive years since 2010, the world's central banks have been net buyers of gold. But from 2022 onwards, the pace became extraordinary. Central banks bought 1,136 tonnes in 2022 - the most since records began in the 1950s. They followed that with 1,051 tonnes in 2023 and 1,045 tonnes in 2024. Even in 2025, when prices were at historic highs, they still bought 863 tonnes - nearly double the pre-2022 annual average.

To put that in context: annual global gold mine production is roughly 3,500 tonnes. Central banks are absorbing approximately one quarter of all new supply coming out of the ground - every single year.

The leading buyers are China, Poland, Turkey, India, and Kazakhstan. Their motivations differ in emphasis but share a common thread: reducing exposure to Western financial systems, particularly the US dollar. China, notably, has been buying gold for 15 consecutive months as of January 2026, simultaneously reducing its holdings of US Treasury bonds from a peak of $1.3 trillion in 2013 to around $683 billion by late 2025 - a deliberate, decade-long portfolio rotation from paper dollar assets into physical gold.

Central banks view gold accumulation as insurance against potential economic warfare, sanctions regimes, and the evolution of the multipolar monetary system. - World Gold Council Central Bank Survey, 2025

The geopolitical engine

To understand why all of this accelerated so sharply after 2022, you need one date: February 24, 2022 - the day Russia invaded Ukraine.

Within days, the United States, European Union, and their allies took an action without modern precedent: they froze roughly $300 billion of Russia's foreign exchange reserves. Dollar holdings, euro holdings, assets sitting in Western financial institutions - all of it locked with a keystroke.

The message this sent to the rest of the world was electric. It was not just Russia that noticed. Finance ministers and central bank governors across the Global South - in countries that have no particular sympathy for Moscow - sat up and asked the same question: if this can happen to Russia, could it happen to us?

Gold cannot be frozen. It cannot be sanctioned. If you hold it in your own vault, on your own soil, it is yours unconditionally. The repatriation of gold reserves accelerated almost immediately.

India's case is particularly striking. In 2024 and 2025, the Reserve Bank of India quietly flew 214 tonnes of gold home from the Bank of England - the largest repatriation since 1991. That year, India had been forced to pledge gold to the Bank of England as collateral for an emergency loan during a balance-of-payments crisis. The humiliation was so deep that it triggered a national economic reform programme. Bringing the gold back, by stealth and in specialised aircraft, was a completely different kind of statement. India's gold holdings now account for over 9% of its total foreign reserves, up from 8.1% just a year prior.

This pattern is happening globally. A 2024 survey found that 68% of central banks now keep most of their gold within their own borders - up from roughly 50% in 2020. The world is quietly repatriating its gold.

Meanwhile, in October 2025, BRICS nations launched a pilot settlement currency called "The Unit" - pegged to one gram of gold, backed 40% by physical gold and 60% by a basket of BRICS currencies. It is designed for international trade settlement between member states, routing around the dollar entirely. Whether it gains traction is a separate question for Part 3. But its existence tells you something about the direction of travel.

Silver's wilder ride

Why Silver Prices Are Soaring | CNBC Explains

Gold stole the headlines, but silver had an even more extreme year. Silver started 2025 at around $30 per ounce and ended it near $77 - a gain of roughly 145%, more than double gold's performance. At its January 2026 peak, silver briefly touched $121 per ounce.

Silver is structurally different from gold in ways that made this move both predictable and dangerous. It is smaller, thinner, and far more volatile. But the key distinction is this: silver is simultaneously a monetary metal and an industrial one. Roughly half of silver demand comes from industrial applications - solar panels, electric vehicles, electronics, and increasingly, AI infrastructure. When both the monetary story (safe haven, dollar hedge) and the industrial story (energy transition, chip manufacturing) align at the same time, silver's response is explosive.

In 2025, both stories were firing. The result was a metal that looked more like a technology commodity than a safe haven - surging in ways that made seasoned traders nervous. As we will see in Part 2, that nervousness was justified.

Where we stood going into 2026

By late January 2026, the mood in precious metals markets had crossed from bullish into something closer to euphoric. Gold had risen 29% in January alone. Silver was up 68% in a single month. Futures positioning was stretched beyond almost any prior recorded extreme. The trade was, in the language of markets, crowded.

Major banks were stumbling over each other with price targets: JP Morgan at $5,000+, Goldman Sachs at $5,400, Deutsche Bank at $6,000, ANZ at $5,800. At least one analyst had quietly published a note suggesting $20,000 was not impossible.

And then, on January 31st, 2026, the market fell off a cliff.

Gold lost 21% in a matter of days. Silver lost 40%. The Warsh appointment lit the fuse. But the powder keg had been packed for weeks.

Part 2: The Crash - coming next.

Sources: World Gold Council Gold Demand Trends 2025; BullionVault Gold News; Investing News Network; JP Morgan Global Research; Deutsche Bank Metals Research; OMFIF; Business Standard; Business Today; Visual Capitalist.